Yes, it’s complicated. Those of us committed to keeping taxing and spending in check have learned it’s complicated and riddled with intended and unintended consequences. As we continue to see the benefits of recent tax and spending reforms, feeling results of recent budgets and contemplating additional reforms – it’s important to consider all options and angles. Particularly when changes to the state’s constitution are being considered, as the General Assembly considered during the 2015-16 session and surely will again during the upcoming 2017-18 session.

During the 2015 General Assembly long session, Senate Bill 607 was filed, proposing state constitutional amendments providing taxpayer protections to limit the growth of spending, establishing a reserve fund with 2% of the state budget each year and limiting the personal income tax rate from 10% to 5%. SB 607 passed the Senate 30 to 15 but was never heard in the House. Senate Bill 817 filed in the first days of the 2016 short session, proposed to cap the state’s income tax rate at 5.5% (reduced from 10%). Yet another effort was made in House Bill 3 in the last days of this year’s short session. Dubbed “Omnibus Constitutional Amendments”, HB 3 included all the aforementioned amendments plus one to protect against eminent domain takings of property and another to protect the right to hunt and fish. HB3 passed the Senate 32-17 but did not get a hearing in the House before sine die adjournment.

So is consideration of constitutional amendments to protect property rights, keep the growth of government in check off the table? We hope not and expect the new General Assembly will consider these and mostly like other ideas as well when they convene in January.

Rep. Skip Stam, with considerable experience and a valiant soldier in the fight to restrain state government from overspending, offered thoughts on constitutionally limiting the state income tax to 5.5%. As we begin to look at tax reform recommendations for the 2017 General Assembly, gathering and considering many ideas, it’s worth looking at Rep. Stam’s thoughts –

What Could Be Wrong with SB 817 Limiting Income Tax to 5.5% Representative Paul Stam

July 2016

The NC GOP platform (Article II) states, “The government should tax only to raise money for its essential functions. We support a thorough review of expenditures each year, and we support a tax payer’s bill of rights.” “Tabor” is the usual acronym for a “Taxpayer Bill of Rights.” A goal I share with proponents of Senate Bill is a mechanism that will restrain state government from overspending.

But does SB817 proposing a constitutional amendment to limit the rate of state income taxation effectuate these principles? Does it expand taxpayer rights or constrict them? And why is it a constitutional amendment?

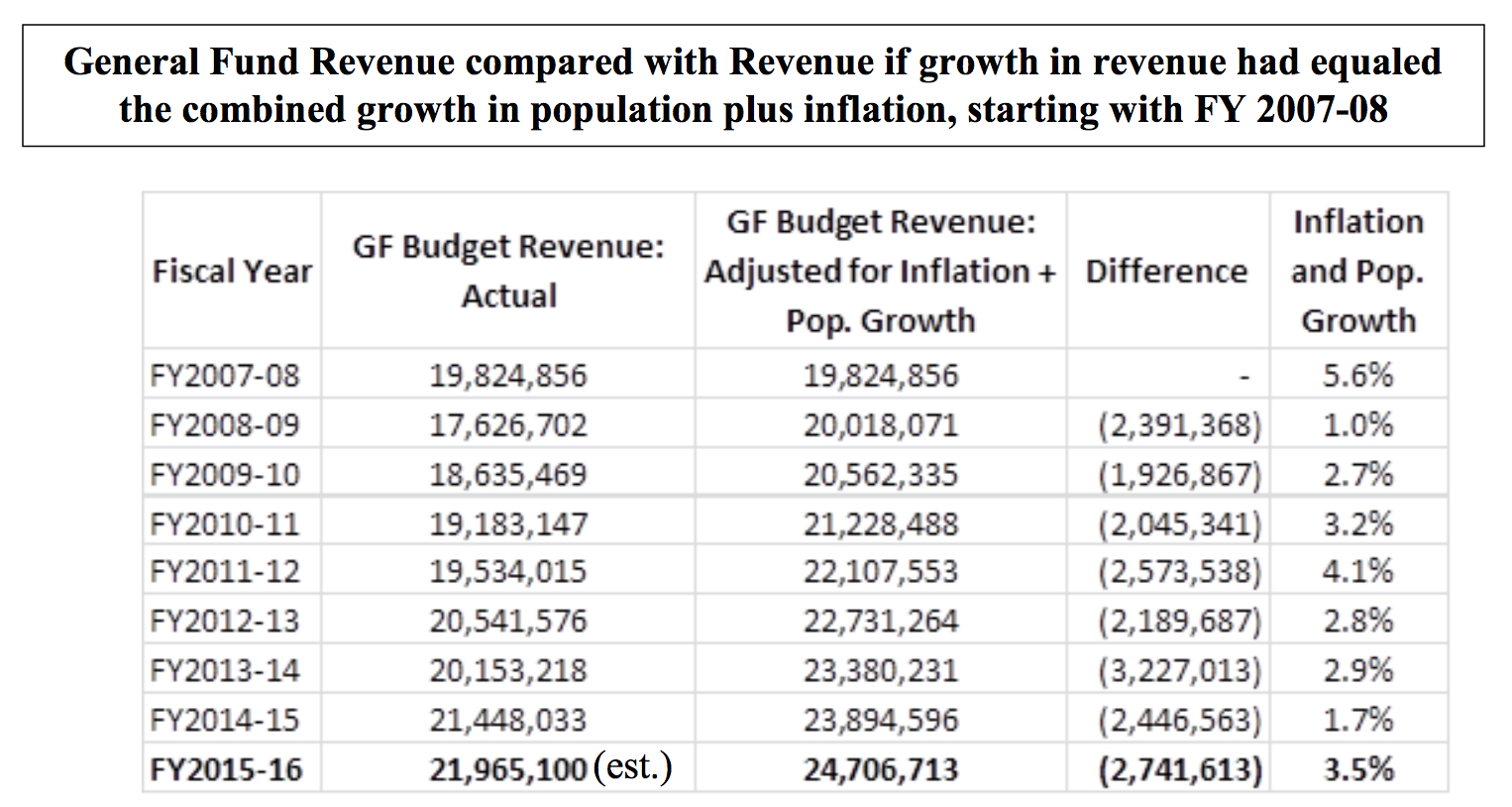

Inflation is a fact and since population changes increase both tax revenue and the need for services, a typical tabor adjusts for increases based on population and inflation. The chart below uses tabor calculations to compare revenues collected in 2007-08 with revenues available for 2015-16.

But the General Fund Budget Adopted for 2016-17 is $ 22,449,487,216, which is more than $3 billion less than what would have been allowed if TABOR had used 2007-08 as the base year.

Before the recession, Democrat budgets typically grew at double the tabor calculated rate from 2001–2008. For example, in fiscal year 2007-08 the calculated tabor rate would have been a 5.6% growth rate but the enacted budget for 2007-08 grew 9.5% over the 2006-07 budget.

The Basic Tabor Problem

The intractable problem with tabor is deciding the appropriate base years. I took the last year in which the Democrats passed the budget they really wanted- 2007-08. After that the recession hit and they were stymied from the summer of 2008 until they lost power in 2011. What the chart shows is that by 2015-16 we collect $3 billion less in revenue compared to what we would have collected if the 2007-08 trajectory had been continued at tabor levels. This is due in part to the recession and in part to the significant tax rate reductions of 2011 (sales and income) and of 2013 (tax reform- primarily reductions in income taxes) and of 2015 and 2016 (more income tax reductions with some base broadening of the sales tax).

The reduction in sales tax rates means that collections are now $562 million LESS in 15-16 than would have been collected under the higher rate but at a narrower base. This is a magnificent achievement and puts the lie to left wing complaints about sales tax reforms hurting the poor.

I am NOT arguing that 2007-08 is the appropriate base year from which the future should be measured. We cut sales tax rates in 2011 even in the depths of the recession and we cut spending and reformed the tax code in 2013, 2015 and 2016. We are $3 billion “short” of where we would have been had the trajectory continued. That is a good thing.

And the Gross State Product is now much larger so the state budget as a percentage of the Gross State Product is now much lower!!! The General Fund spending was 5.5% of state GDP in 2007- 08 and is estimated to be 4.6% of state GDP in 2015-16. This is a 16% reduction in the proportion of the Gross State Product spent in the general fund.

SB817 sought to remedy the spending problem by capping state income tax at 5.5%.

SECTION 1. Section 2 of Article V of the North Carolina Constitution reads as rewritten:

“Sec. 2. State and local taxation. …

(6) Income tax. The rate of tax on incomes shall not in any case exceed ten five and one-half percent, and there shall be allowed personal exemptions and deductions so that only net incomes are taxed.

….”

The amendment would have become effective for taxable years beginning on or after January 1, 2017.

To change that rate would take another constitutional amendment requiring 3/5 of the whole House, 72 votes, and in the Senate, 30 votes plus a referendum.

Why would we want to put the future of the state in the hands of Democrats whose vote to make up the 72 votes may cost us dearly? Why do I say that Democratic votes would be necessary when Republicans have supermajority numbers? The reason is that, even if the supermajority is retained, I would assume that there would always be some Republican votes against raising tax rates, no matter what.

The normal rule is that a majority decides. Why would Representatives and voters of 2016 think that they had superior knowledge of government policy to those of 2017 or beyond? SB817 makes no more policy sense than a liberal version that REQUIRED a minimum level of income taxation.

SB817 also may have a negative effect on our AAA bond rating, as pointed out by the state treasurer. (Please see attached.) The Treasurer’s opinion is just that- an opinion. But bond ratings themselves are just that – opinions. And bond ratings (opinions) matter – a lot. If we lose our AAA rating the cost of borrowing increases.

Particular Problems with SB817

SB817 restricts increases in income tax- not increases in overall state taxes- so it almost requires increases of other taxes. It is no surprise that the Senate plan is to reduce income taxes from 5.49% to 5% while adding to services subject to sales tax!

First, federal tax law allows a tax payer to deduct state income tax or state sales tax, whichever is greater, but not both. 98% of itemizers deduct the state income tax. By swapping a deductible tax for a tax that, for all practical purposes, is nondeductible for 98% of our NC itemizers, SB817 causes a large federal tax increase on our constituents. 2015’s modest tax reform will cost state taxpayers $19 million (annualized) in additional federal taxes. If SB817 becomes law it will cost state taxpayers hundreds of millions of dollars annually in unnecessary payments to Uncle Sam if additional sales taxes are collected as planned.

Second, the problem with trying to squeeze income tax receipts into taxes on services is this: a tax on services is an income tax on gross income. Is that a good idea? A couple of years ago I asked Arthur Laffer if a sales tax on services was really much better than a flat income tax at a relatively low rate. He said “no,” as long as we keep it low and flat.

Third, we have already seen in the 2015-16 Budget one tax replace another to meet a goal. On an annualized basis new taxes and fees of $185,895,000 are in the Highway Funds. Meanwhile $208,659,902 was made available to the Highway Fund by ending longstanding transfers from it to the General Fund. So an apples-to-apples comparison would show a larger increase in spending than advertised.

Fourth, SB817 would encourage more borrowing since receipts from a bond would not count against the tax limitation and the resulting spending could be counted over decades rather than the years the money is spent.

Fifth, SB817 raises a serious practical constitutional problem. Suppose the “sales tax” was extended to the services of a CPA. But what is a sales tax on a pure service but an income tax on gross income? A CPA could refuse to pay the 6.75% “sales tax” claiming that it exceeded the 5.5% constitutional limit. The budget for that year would be in chaos.

The Federal Angle

The massive problem of government overspending is primarily at the federal level- not the North Carolina state level. At the federal level, we are more than $19 trillion in. On the books the annual federal appropriation is now $3.7 trillion and is over 20% of GDP.1

Someday a responsible Congress will meet a responsible President and come to a “Grand Bargain” on spending. Suppose that “Bargain” included a $1 trillion dollar reduction in federal spending. $900 billion would not be spent at all. The other 10% ($100 billion) would be devolved to the states to cover functions that truly belong to the states but have been hijacked by the feds. Education and some transportation funding come to mind. Conservatives would be in a state of delirious joy!!

But that “Grand Bargain” would require a $3 billion increase in North Carolina state revenues. Taxpayers would be delighted because of the corresponding huge reduction in the federal tax and debt burden. But it would be virtually impossible for NC to take up the offer if SB817 were part of our Constitution. Democrats would impose impermissible demands as ransom for the votes necessary to revise the Constitution.

Two Practical Solutions

Fortunately, there is a practical solution. The Budget Reform Act of 2013 would put the mechanism in play to make over-taxation and overspending difficult. This proposal is based on a bipartisan proposal by Representative Art Pope and Senator Bill Goldston in 1991. It is time for the General Assembly to pass it.

In the meantime, electing Republican majorities since 2010 have resulted in more restraint on spending and taxation than a constitutional limit on income tax ever would.

1 https://www.cbo.gov/sites/default/files/114th-congress-2015-2016/graphic/51110-budget1overall.pdf.